Certainty is the New Trade Currency

Supply chain rerouting, extra industrial taxes, and how to deal with fickle trade partners

We are only days into Quarter 2 of 2026, and this year has proven to be the year of unprecedented events, which will set up precedents for years to come.

In our own materials/manufacturing/industrial world, fundamental changes are also happening. The industrial formula used to be straightforward: minimise unit cost, stretch your supply chain across the globe, and assume that lanes stay open and energy is stable.

That math is now being challenged by a chain reaction of the 3 following events.

1. Several chokepoints → supply chain rerouting

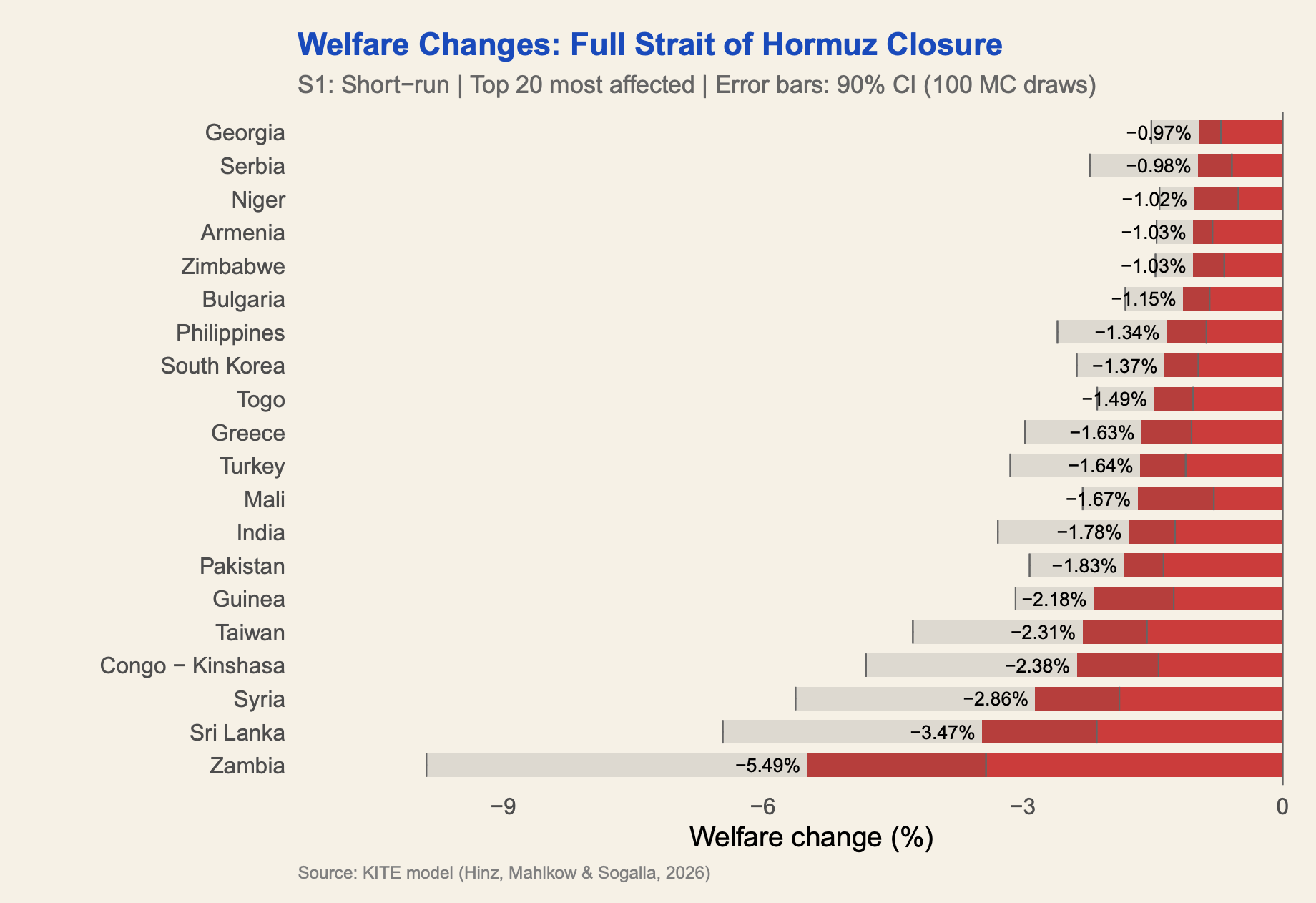

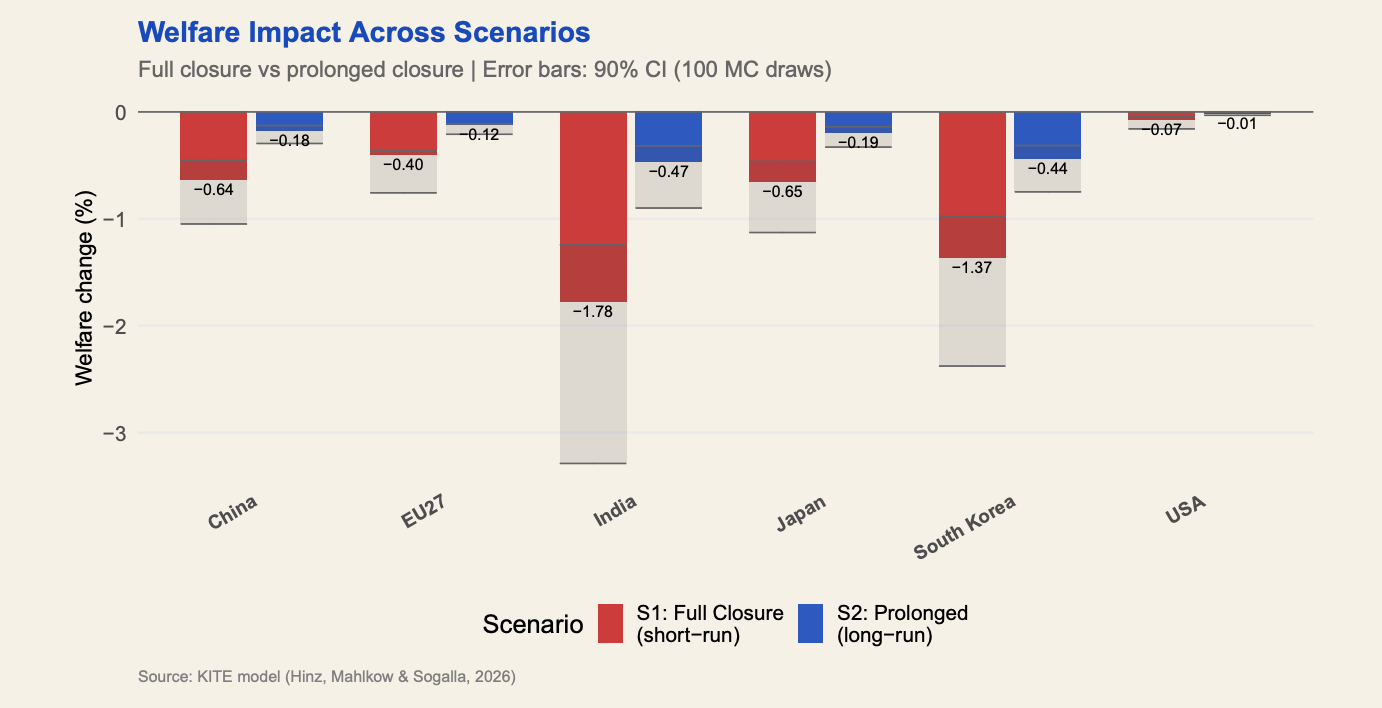

The industrial world has been closely monitoring the closure of Hormuz since February 28. The first impact has been observed: oil prices surge, then raw materials and feedstock prices surge.

In the study “The Cost of Closing the Strait of Hormuz: Energy Bottlenecks and Global Food Security”, researchers from Kiel Institute for the World Economy (Germany) stated that “A prolonged closure allows some market adjustment, but structural damage persists - and the timing during peak Northern hemisphere planting season compounds the food security risk.”

Interestingly, researchers from Kiel stated that “At every point in the value chain, some substitution is possible, which is precisely why the long-run scenario shows smaller effects.” This is what we call the Dangerous Calm of Hormuz - where the structural cost of rerouting supply chains will settle in the next 2 to 6 months.

Yet, rerouting supply chains is much more complex, given other complications elsewhere. The Bab-el-Mandeb Strait / Red Sea crisis due to Houthi attacks on commercial vessels has rerouted global logistics since late 2023. Despite a reduction in attacks in 2025, thanks to ceasefire arrangements, traffic through the Red Sea and Suez Canal remains below pre-crisis levels: transits in 2025 fell to around 35–40% of 2023 volumes, and Suez Canal traffic in early 2026 remains around 60% lower. The Cape of Good Hope is now the new route for Asia-Europe freight, which means +10 to 14 days, and +20-30% fuel consumption.

On April 9, Time reported that Iran is considering restrictions on the Bab-el-Mandeb Strait again, amidst negotiations with the Trump administration.

2. Tighten Regulations: Extra industrial taxes → thinner margins

On April 7, 2026, the European Commission published the first official CBAM certificate price, €75.36 per tonne of CO2 for Q1 2026. The CBAM definitive phase began on January 1, 2026, covering iron and steel, aluminium, cement, fertilisers, hydrogen, and electricity, but certificate purchasing starts in February 2027.

Who is winning and losing with CBAM?

From 2026, free allocations under the EU ETS (Emission Trading System) are being phased out. By 2031, European producers will pay for roughly 64% of their scope 1 emissions out of pocket (see the chart above). What CBAM does is ensure non-EU exporters face the same trajectory at the border. Without it, cheap, carbon-heavy imports would undercut producers already paying into the system. So European producers do get protection from foreign competition and a rising cost burden at the same time. The playing field levels - but at a higher floor for everyone.

3. Fickle Trade Partners vs Calm Ones → Certainty is the New Currency

In trading, the most important thing is trust.

And it is not easy to trust a trade partner that unilaterally imposes “reciprocal” tariffs with no notice, and on another random Monday, self-imposed an online feud with Pope Leo XIV, head of the Catholic Church. (The list could be much longer, but was kept short for the sake of noise reduction.)

When facing such a trade partner, one naturally will diversify and look for calmer, more predictable ones. From April 11 to April 14, Spain’s PM Pedro Sanchez paid an official visit to China, the 4th time within 4 years, as he sought to "narrow Spain’s trade deficit of nearly $50 billion with Beijing. The exact measures are to be communicated.

On April 14, General Secretary of the Communist Party of Vietnam (CPV) Central Committee and State President To Lam arrived in Beijing, beginning the state visit to China. Key areas of discussion will include trade, investment, supply and production chains, education & training, and science & technology.

In an increasingly uncertain world, certainty and trust are the new currency of trade and collaboration. Not cost, not trade volume.

This is what our team believes in.

And we do our own effort of building trust in our global network of material and manufacturing.

Our effort of trust building: Verified Buyers matching with Verified Suppliers

Instead of bouncing between supplier sites, trade show floors, PDFs, and cold outreach - none of which truly build trust and certainty - MatterDrop is being built as a more curated, higher-signal experience: curated material themes, with available samples, brochures, and supplier profiles available in one place.

Every week, “fresh” new sample (and/or brochure) Drops of the Week are made available to MatterDrop’s approved early users.

Access is opening gradually. The first wave is intentionally limited. Application open now. Check out to claim your free (verified) samples.

A Step Further ⋅ Private Executive Immersion into China’s Industrial Frontiers

If China is part of your strategic horizon, the natural next step is FutureMade China - a private, curated, executive immersion for those who want to see the terrain directly.

The current concept for the next cohort is a 5-day route through Beijing, Suzhou, Shanghai, Nantong and beyond, designed for founders, investors, and senior operators seeking direct access to China’s industrial frontier across advanced manufacturing, robotics, AI, biomanufacturing, industrial policy, and the systems shaping what comes next. Applications are now open for the June and October 2026 cohorts.

FutureMade is not a tour. It is a private executive immersion into China’s industrial frontier. Each cohort is intentionally kept very small to preserve the quality of access, conversation, and fit.

Even More Resources for You

(Global 🌏) “Sourcing Electronics from China and Vietnam in 2026”, a report by Tocco on consumer hardware, PCBs, and EV batteries across both countries, with verification procedures, tariff analysis, and risk & compliance checklists for procurement teams.

(Global 🌏) “The New Twin Fossil Shock”, a report by Ember on “how the energy crises of the 2020s speed up the electric age”. More developments to be observed still - we keep a close look at this in the next quarters.

(Global 🌏) Top 10 Brands Embracing Monomaterials in 2026. Monomaterial design is moving to a compliance requirement; our team looks at 10 brands across industries that have started to make the shift.

(US 🇺🇸) John Deere to pay $99 million in a right-to-repair lawsuit. The tractor maker is paying for its years as the central opponent of right-to-repair. Consumer advocates say it’s still not enough.

(China 🇨🇳) China to ban Sulfuric Acid exports as War hits supply. Sulfuric acid is both produced by smelters and consumed in the mining industry