Hormuz's False Calm

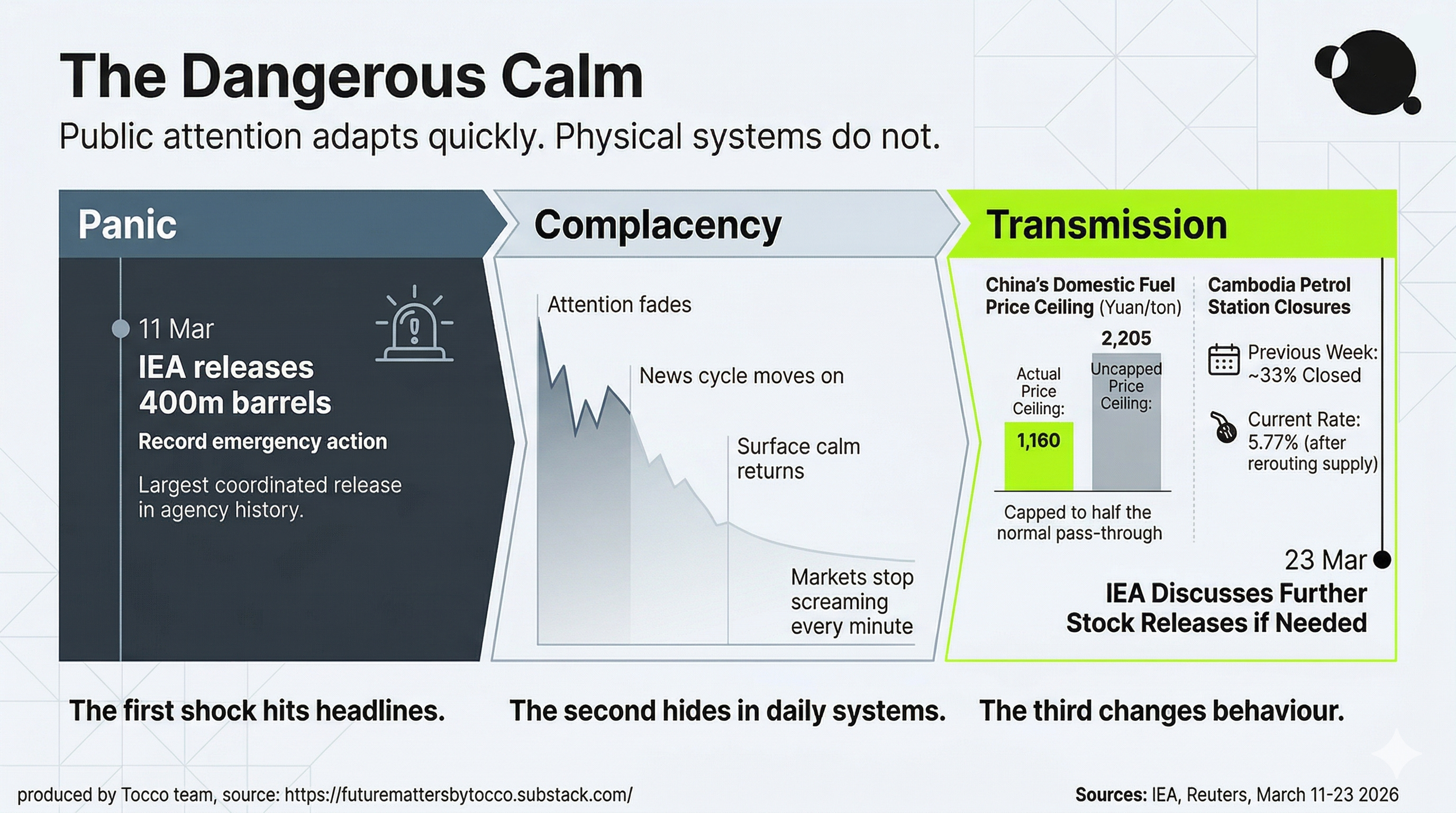

Panic comes first. Then complacency. Next thing we know is the economy starts to break.

24 days into a war, modern media has moved on.

For the first 48 hours, you can find maps, missiles, oil price hikes, and all matters of crisis. And then, everything just became white noise in the background. People started talking as if the worst was behind them.

Spoiler alert: it isn’t. The global supply chain moves a hell of a lot slower than social media, and the Hormuz blockage is simply the first domino to fall.

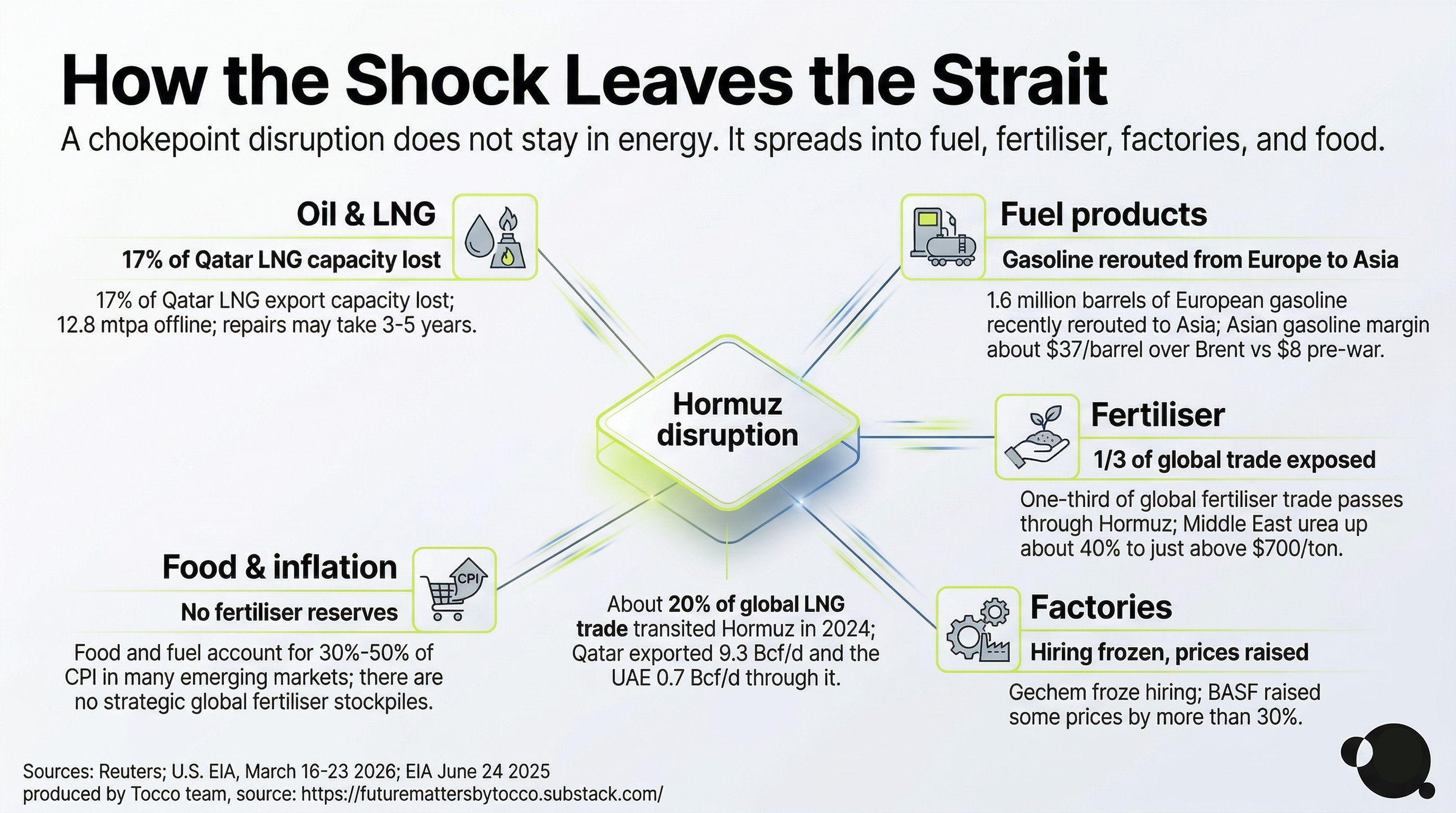

People still think of “oil” when they hear Hormuz. That’s not wrong, but it doesn’t cover everything that entails. Crude oil is much more than just fuel. It is the lifeblood of the global economy.

Take a look at headlines beyond the Western hemisphere, and you’ll immediately see the ripples. I would describe the past ten days not as a crisis that has calmed down, but as a public that has moved on faster than a system can stabilise.

As a matter of fact, it is still a war zone out there. Trump has threatened to strike Iranian power infrastructure if Hormuz is not reopened. Iran has threatened Gulf power and water infrastructure in response, while saying some shipping may pass only under its terms. The IEA is already discussing whether further oil stock releases may be needed after the record 400 million barrel release earlier this month.

That is still only the first wave. The second one is about almost everything that relies on crude oil and open trade routes.

Take LNG. Reuters reports that Iranian attacks have wiped out 17% of Qatar’s LNG export capacity, with repairs potentially taking three to five years. That’s enough to steer strategies off track. ADNOC (Abu Dhabi National Oil Company) in the UAE is also adjusting LNG output because of shipping disruption, while European policymakers have been forced back into gas-security mode. The phrase “temporary disruption” becomes harder to use with a straight face when the damage may last longer than some business plans.

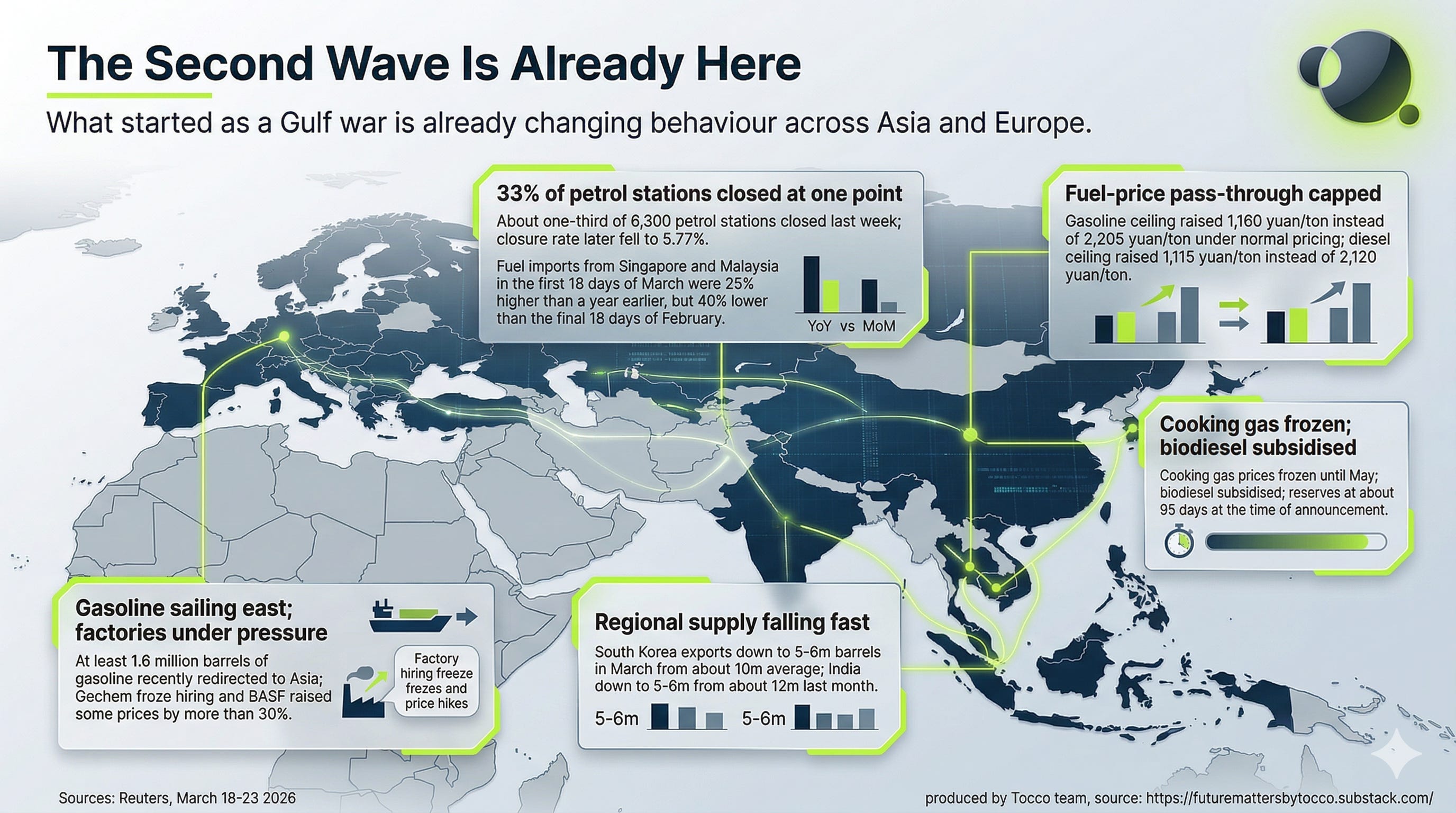

Next, crude oil. It can be an abstract idea to many people, but diesel, gasoline, and jet fuel aren’t. In fact, many Asian nations have felt the effects of the war in their daily lives.

In Cambodia, roughly a third of petrol stations closed at one point before emergency supplies reduced the closure rate.

Vietnam has accelerated its shift to E10 fuel rather than sticking to its timetable.

Thailand has moved to freeze some cooking-gas prices and promote subsidised biodiesel.

China has limited how much of the global fuel shock gets passed through domestically.

Europe is now sending gasoline east, because Asia has cut down massively on their exports. The global market is actively redefining how refined oil products are traded, rather than simply repricing them. This means higher transport costs, worse distribution, and more pressure on consumers and manufacturers.

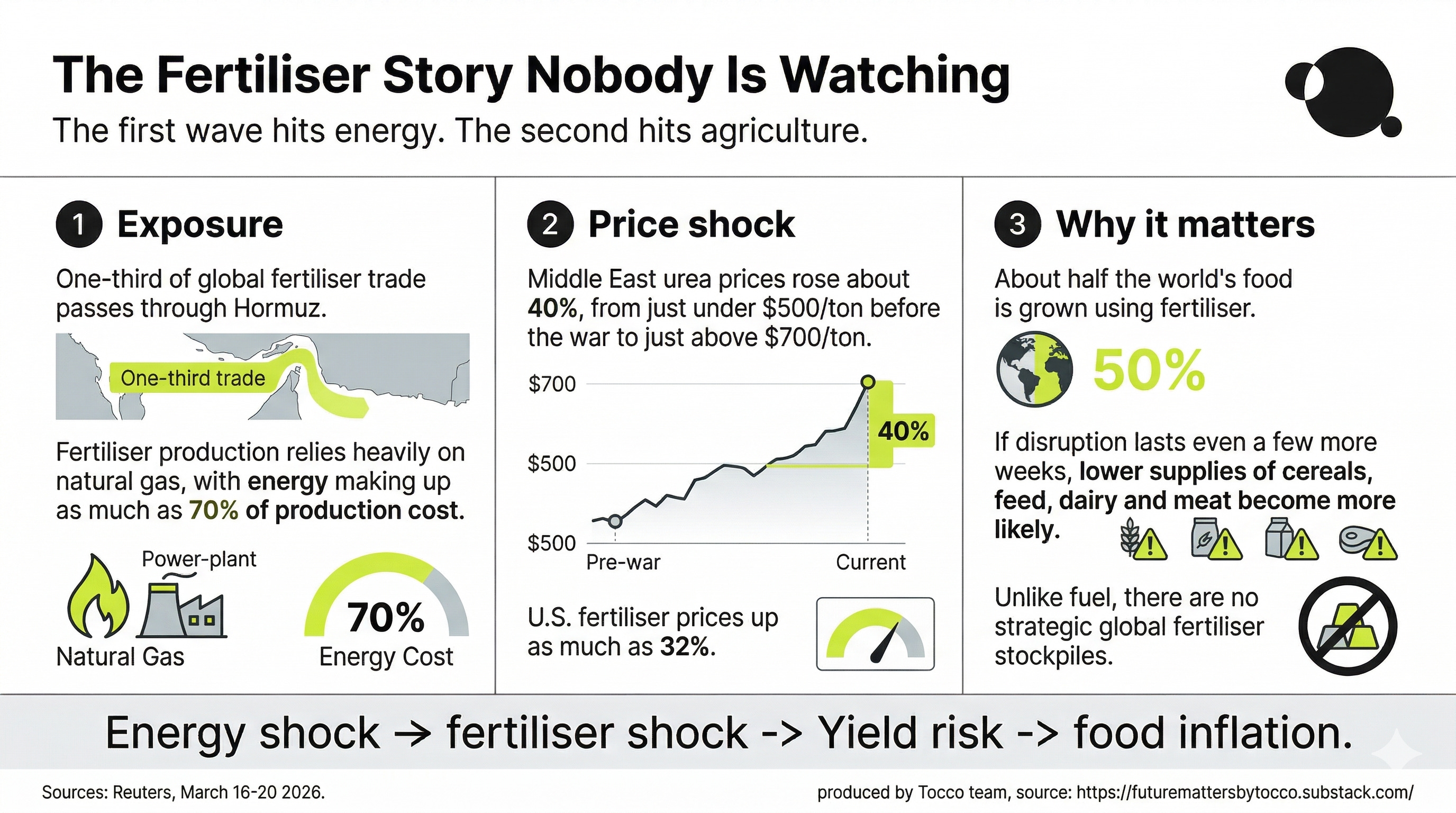

Then comes the silent killer, in the form of fertiliser.

Reuters reports that roughly one-third of global fertiliser trade passes through Hormuz. Middle Eastern urea prices have already risen about 40%, U.S. prices about 32%, and production has been halted or disrupted in multiple countries. There are no strategic fertiliser reserves equivalent to oil stockpiles. That means no Plan B here, contrary to popular assumptions. If the disruption persists, we will see it in delayed planting, lower yields, and a fresh food-price shock that will hit poorer importing countries first and hardest.

By the time the headlines feel old, the consequences have already made themselves known through fuel, fertiliser, food, and factories, slowly but surely. This is how modern shocks work - slow and hidden, yet they pack a powerful punch.

Sooner or later, the public will feel it in their grocery lists, their energy bill, their takeaway lunches, and will be none the wiser until it's too late.

Europe is already feeling the industrial version of this. Reuters reports that companies across Germany and the wider industrial Europe are freezing hiring, raising prices, delaying investment, and reconsidering production plans due to higher energy and raw material costs. BASF, Henkel, Evonik, and other manufacturers are again being pushed into defense. Some Asian suppliers are invoking force majeure. This is not just bad news for commodity traders, but also for designers, buyers, product teams, CFOs, and founders who still believe geopolitical shocks remain safely outside the walls of their business unless they are in oil and gas.

Stay with me now:

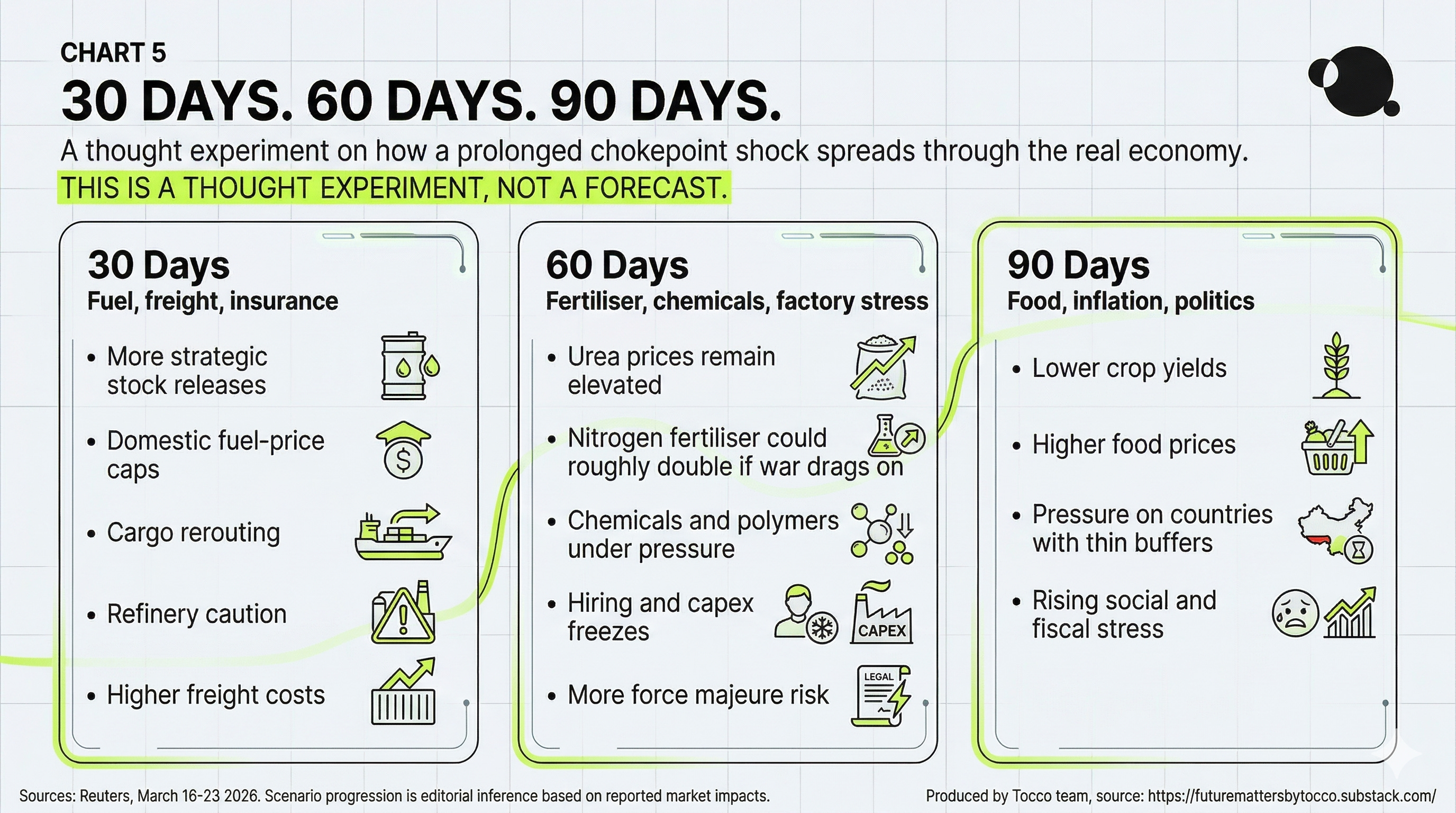

If Hormuz disruption lasts another 30 days, this remains mainly a fuel, freight, and insurance story.

If it lasts 60 days, it becomes a much broader fertiliser, chemicals, and industrial-input story.

If it lasts 90 days, it starts becoming a food, inflation, and political-stability story in the most vulnerable countries.

I’m only making educated guesses, of course. The already-visible data: first shipping and energy, then fuel products, then farm inputs, then food systems, then politics.

This is why the most misleading signal in the world right now may be the surface calm that follows the storm. It’s much easier for people than systems to recover.

Which, in turn, creates a dangerous calm for all parties involved.

I’m not seeing things from a militaristic lens, but one that’s industrial. I grew up in China, spent years in Europe, and have lived close enough to manufacturing, supply chains, and cross-border systems to know that physical consequences usually arrive later than emotional ones. People will feel fear and fatigue long before they face reality.

That is what Shockwatch is for. We are not trying to out-report foreign correspondents, nor compete with the noise machine. We are only tracking how geopolitical shocks affect decision-making before firms have to pay.

Stay tuned for more.

Trust me, there will be, unfortunately.

Leon Ge

23 March 2026

* The name “Hormuz” is a linguistic descendant of Ahura Mazda, the Zoroastrian god of light and wisdom. It evolved over centuries from the Middle Persian forms Ohrmazd or Hormoz into the name we recognize today.

Why we publish this

FutureMatters exists to help busy teams understand how the physical world is being redesigned by conflict, rules, machines, materials, trade, and industrial strategy.

About the author: Leon Ge writes and builds at the intersection of AI, manufacturing, regulation, materials, and industrial strategy. He is the founder of Tocco.

Subscribe to get the next issue of Shockwatch and the weekly FutureMatters brief. You can also follow Leon on LinkedIn for shorter notes and field observations.

Private invitation: FutureMade China

A small group of founders, investors, and senior operators will join us in 2026 for a closed-door immersion into China’s industrial frontier - from advanced manufacturing and robotics to AI, biomanufacturing, and the ecosystems shaping the next decade. If you want to see the China that most executives never get access to, apply for an invitation here.