Switching Positions – Trump vs Wind, Critical Minerals & The New Orders #208

$1 billion to stop wind power, Hormuz's false calm, critical minerals, high virgin plastic price and sourcing in China and Vietnam

Five stories that matter this week:

The White House agreed to pay TotalEnergies $1 billion to walk away from its East Coast offshore wind projects - and redirect that capital into US LNG production instead (four trains at the Rio Grande LNG plant in Texas, plus upstream oil in the Gulf and shale gas). In return, the US reimburses them dollar-for-dollar on their original wind lease purchases. As part of the deal, TotalEnergies has pledged not to develop any new offshore wind in the US.

The timing is aligning. With Hormuz disrupting global oil and gas supply, the US - the world’s largest LNG exporter - is positioning itself as the critical supplier on both the Europe and Asia fronts. Europe needs it to replace Russian pipeline gas. In Asia, buyers like China, Japan, and South Korea can resell US cargoes freely - no destination restrictions - effectively acting as the world’s most flexible energy middlemen.

We’ve said it before: from afar, watching US policies is like watching a sport with a winner's name changing every season (aka mandate). Wind was the future some years ago. Now it’s “one of the most expensive, unreliable, environmentally disruptive schemes ever forced on American ratepayers,” according to the DOI.More on Hormuz, it all seems like white noise in the background now (arguably, less animated than the debate around Melania Trump and the educator humanoid robot). Leon, Tocco’s founder, argues that the worst for the global supply chain is yet to come: beyond 60 days, the situation becomes a chemical and industrial-input story; beyond 90 days, it becomes a food, inflation, and political stability story. You can read Leon’s full analysis of what he calls “The False Calm” here. If you want to discuss at length with Leon about supply chain, industries, or geopolitics - feel free to ping him at leon(at)tocco.earth.

Speaking of critical resources, we published this week, Toccographic “Critical minerals are the new oil”. We discuss how the world is shifting from a fuel-based economy to a mineral-intensive one, with several monopolies creating bottlenecks for the supply chain, and that the future might depend on advanced recycling and urban mining - not just digging bigger holes in the deep ocean or in asteroids.

At the same time, a pricing signal in plastics: the price of virgin PET bottle-grade resin has spiked due to a combination of $100+ oil prices and supply chain shocks in Hormuz, so much so that the price of virgin PET is now nearly equal to the price of recycled food-grade pellets in Northwest Europe.

Historically, recycled plastic has been much more expensive than virgin plastic, but the price gap is now at its narrowest point since May 2018.

This potentially could change the procurement calculus: companies avoid recycled plastic because it is more expensive, but now that the “extra cost” for using recycled content has quite disappeared. It is, however, still anyone’s guess if this price gap will last. We will follow this story further.Speaking of procurement, this week’s guide is on Sourcing in China & Vietnam 2026. We cover the current tariff landscape, how to compare manufacturing capabilities between the two countries, and the operational risks that eat into your margins: quality fade, middleman structures, and communication failures. Download this practical guide if this is your space.

Enjoy your weekend. Stay sharp - and keep building.

Anh

On behalf of the Tocco team

Deep Read of the Week: Europe’s True Reindustrialisation - First, Look Into the Abyss

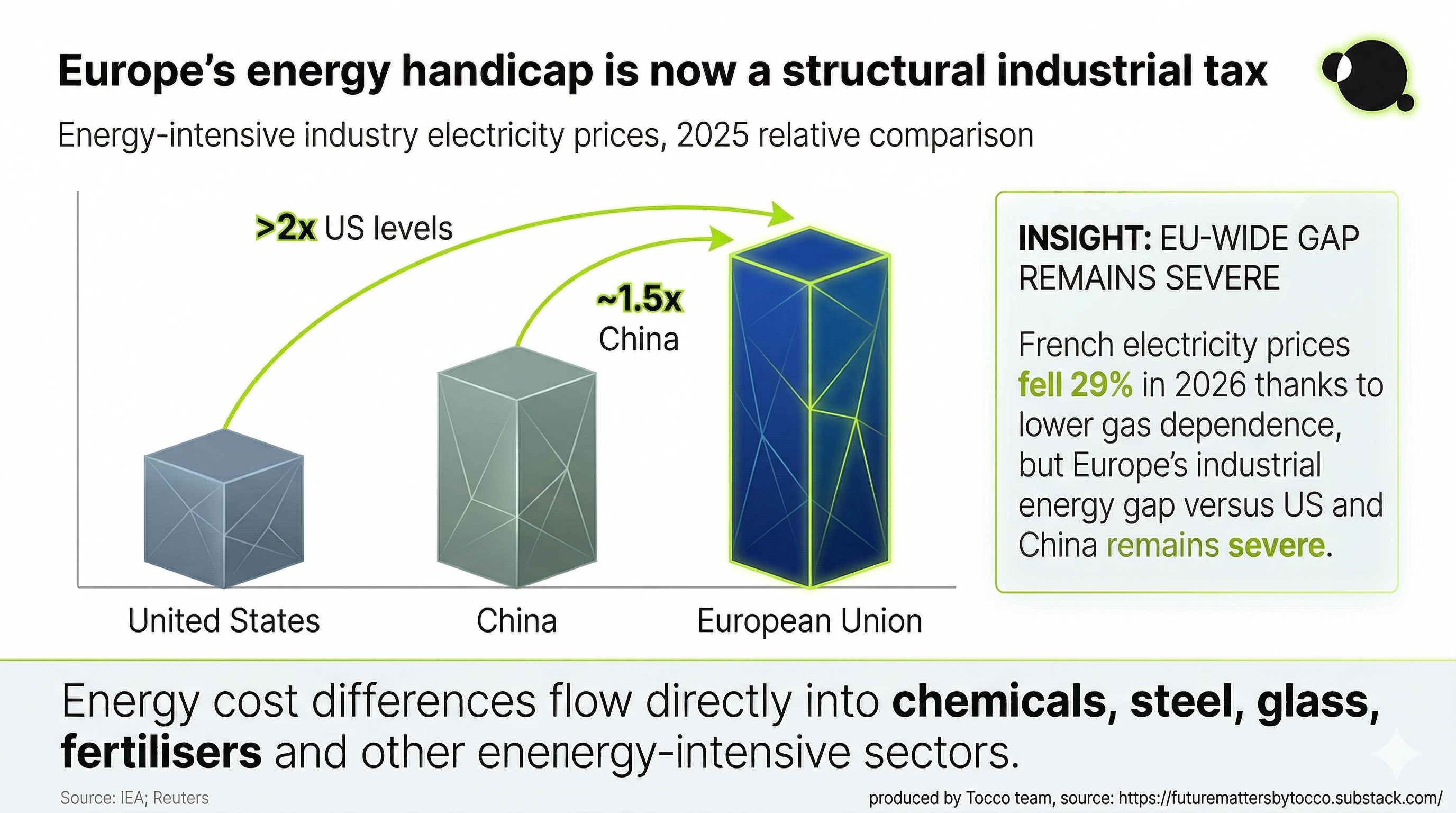

If Europe wants the great reindustrialisation, it needs more than speeches. In this analysis, Leon argues that the industrial cards are not in the EU’s favour: industrial production averaged just 0.6% annual growth between 2000 and 2024. Energy costs for industry remain more than double US levels. European steel production hit a historic low in 2025. But there is no time to despair.

In his view, Europe’s problem is not a lack of excellence. The situation could still be turned around. But first, one needs to look at the reality.

Matterdrop - we’ve been testing something new.

Over the past months, one pattern kept repeating across conversations with both material buyers and suppliers in our network: the hardest part is not interest, but matching the right demand with the right supply at the right moment. So we built MatterDrop. A lightweight layer on top of Tocco that allows:

Buyers to surface real, structured demand signals

Suppliers to access early, high-intent opportunities

For Buyers: If you are looking for specific materials, capabilities, or innovations -

MatterDrop lets you broadcast targeted demand and get matched with relevant suppliers. → Submit a demand signal here ←

For Suppliers: If you are building materials, processes, or technologies that deserve visibility - MatterDrop gives you access to curated demand streams you won’t find publicly. We are keeping this intentionally small in the beginning, as signal quality matters more than volume at this stage. → Get early access to demand here. ←

Further Readings · Material & Manufacturing News · 03.2026

(Europe 🇪🇺 x Austrlia 🇦🇺) After nearly a decade of negotiations, the EU and Australia concluded a free trade agreement. Over 99% of tariffs on EU exports to Australia will be removed, with EU exports of goods expected to grow by 33% over the next decade, saving EU exporters roughly €1 billion a year in duties. The deal also improves access to critical raw materials and includes a Security and Defence Partnership.

(China 🇨🇳) A new lifecycle assessment compares battery electric and gasoline vehicles across China’s six regional grids, factoring in seasonal battery degradation at real temperatures. In Heilongjiang, where winter averages hit -16.3°C, charging efficiency drops to 59%, and the annual emissions advantage over gasoline compresses to just 14.2%.

(Burkina Faso 🇧🇫) Burkina Faso imported 710 high-performing pregnant cows from Brazil, producing up to 40 litres of milk per day, compared to 0.5–1.3 litres from local cattle. The goal: improve herd genetics, build a domestic dairy factory, and cut annual dairy imports currently costing 20–22 billion CFA francs ($35-38 million).

(Global 🎮) Nintendo cut Switch 2 production by a third, from 6 million to 4 million units, after overestimating US holiday demand. A memory market crisis also pushed up production costs. The recent release of Pokémon Pokopia has revived American buying, but Nintendo is waiting for stable demand before scaling back up.

(China 🇨🇳) Chinese scientists have developed a hydrofluorocarbon-based electrolyte that enables lithium batteries to exceed 700 Wh/kg at room temperature and maintain 400 Wh/kg at -50°C - a threefold increase in energy storage that could push EV range past 1,000 km per charge. If this is your space, read more on China’s EV production landscape and its full-loop ecosystem.

(Global 🤖) If Collaborative & Industrial Robotics are in your space, we’ve made a summary of where cobots stand in 2026: built to handle the dark, dull, dirty, and dangerous work alongside humans, no safety fencing needed.

Private invitation: FutureMade China

A small group of founders, investors, and senior operators will join us in 2026 for a closed-door immersion into China’s industrial frontier - from advanced manufacturing and robotics to AI, biomanufacturing, and the ecosystems shaping the next decade. If you want to see the China most executives never get access to, apply for an invitation here.